By : GA Consulting 28 April, 2026

Every year, salaried employees across India wait for their Form 16. It's the document that kicks off tax filing season — the TDS certificate from your employer that confirms what you earned and how much tax was deducted. Most people have been doing this long enough that checking for Form 16 is almost muscle memory.

Starting 1 April 2026, that form will be called Form 130.

The change is part of the Draft Income Tax Rules under India's new Income Tax Code — a broader modernisation effort that renames several commonly used tax forms. The purpose of each form stays exactly the same. The numbers on the tin change. That's it.

Simple as it sounds, these kinds of changes cause real confusion during filing season — especially when employees, employers, and accountants are all working from different reference points. This post gives you the complete picture, with clear before-and-after mappings for every form that's changing.

India is in the process of replacing the Income Tax Act, 1961 with a new Income Tax Code. The new Code aims to simplify the language, structure, and administration of tax law — reducing the complexity that has built up over six decades of amendments and additions.

Part of that simplification involves renumbering and reorganising the forms used across the tax system. The old numbers — 16, 16A, 26AS, 24Q, 26Q — were assigned over years without a consistent logic. The new numbers follow a structured sequence that maps more cleanly to the Code's internal organisation.

Nothing about what these forms do is changing. The rename is administrative housekeeping — but housekeeping that will affect every salaried employee and employer in India from FY 2026-27 onwards.

Here is every form that is changing, effective 1 April 2026:

| Old Form | New Form (Apr 2026) | Who It Applies To | What It Is |

|---|---|---|---|

| Form 16 | Form 130 | Salaried employees | Annual TDS certificate from employer |

| Form 16A | Form 131 | Non-salary recipients | TDS certificate for contractor fees, rent, commission etc. |

| Form 26AS | Form 168 | All taxpayers | Annual Tax Credit Statement — shows all TDS, TCS, advance tax against your PAN |

| Form 24Q | Form 138 | Employers (filing) | Quarterly TDS return for salary payments |

| Form 26Q | Form 140 | Employers (filing) | Quarterly TDS return for non-salary payments |

Keep this table. Share it with your payroll team, your accountant, and anyone in your organisation who handles tax documentation. It will save time when queries come in during filing season.

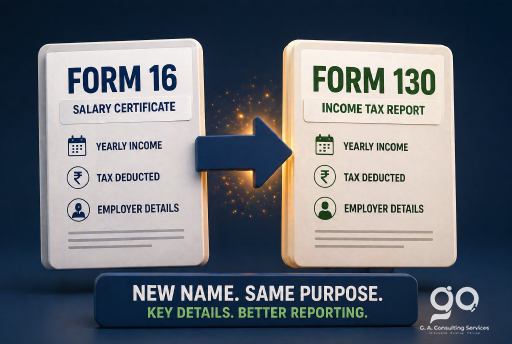

Form 16 is the most widely used tax document in India. If you're salaried, your employer issues it every year after the financial year ends — typically by 15 June. It has two parts: Part A, which shows the actual TDS deposited with the government, and Part B, which gives the detailed salary breakup.

From FY 2026-27, this document will be issued as Form 130. The content, the two-part structure, and the issuing deadline are all unchanged. Only the name changes.

What this means practically: when you sit down to file your ITR for FY 2026-27, look for Form 130 from your employer, not Form 16. If your employer's payroll system or HR portal still shows 'Form 16', raise it with your HR or finance team — their systems should be updated by then, but early filing season is when these gaps tend to surface.

Form 16 (old) = Form 130 (new). Same document. Same information. Same purpose. New name.

Of all the forms being renamed, Form 26AS getting a new identity as Form 168 deserves the most attention — because this is the document most people check without fully understanding what it is.

Form 26AS is your Annual Tax Credit Statement. It's linked to your PAN and shows every rupee of tax that has been deposited against your name — TDS deducted by your employer, TDS on interest from your bank, TCS collected on purchases, any advance tax you've paid, and self-assessment tax payments. It's essentially the government's record of your tax account.

Before filing any ITR, the single most important verification step is to cross-check the figures in your salary documents (Form 16 / Form 130 from FY 26-27) against your tax credit statement (Form 26AS / Form 168 from FY 26-27). Mismatches between the two are one of the most common causes of income tax notices.

Under the new numbering, this statement will be called Form 168. The data it contains, the way you access it (through the Income Tax portal under your PAN login), and its role in the filing process are all unchanged.

Not everyone's income comes from a single employer. If you've received contractor fees, professional service payments, rent income, commission, or interest payments where TDS was deducted by the paying party, you'd have received Form 16A as your TDS certificate.

This form becomes Form 131 from April 2026. Banks, companies, and other deductors who issue TDS certificates on non-salary payments will issue Form 131 going forward. If you receive income from multiple sources with TDS deducted, you may receive several Form 131 certificates from different deductors.

The process for reconciling these against your Form 168 (the new 26AS) remains the same.

These two are primarily relevant to payroll and finance teams rather than individual employees, but understanding them matters for anyone who oversees tax compliance in an organisation.

Form 24Q becomes Form 138

Form 24Q is the quarterly TDS return that employers file for salary payments. It captures details of TDS deducted from employee salaries in each quarter and is the basis on which the government reconciles TDS credits in employees' tax accounts. Under the new rules, this quarterly filing will be done using Form 138.

Form 26Q becomes Form 140

Form 26Q is the equivalent quarterly return for non-salary TDS — covering contractor payments, professional fees, rent, interest, and other specified payments. This becomes Form 140 from FY 2026-27.

For employers, the critical point is that payroll software, TDS filing systems, and internal compliance templates will all need to be updated before the first quarter filing of FY 2026-27. The filing deadlines remain the same; only the form numbers change.

For employees and individual taxpayers

| You Used to Look For... | Now Look For... | When You Need It |

|---|---|---|

| Form 16 | Form 130 | When your employer issues your annual TDS certificate |

| Form 26AS | Form 168 | Before filing your ITR — to verify all tax credits |

| Form 16A | Form 131 | If you received contractor fees, rent, or professional income with TDS deducted |

For employers and payroll / compliance teams

| Old Form | New Form | Filing Obligation |

|---|---|---|

| Form 24Q | Form 138 | Quarterly TDS return for salary payments — file within 31 days of quarter end |

| Form 26Q | Form 140 | Quarterly TDS return for non-salary payments — same filing deadlines apply |

| Form 16 | Form 130 | Issue to each salaried employee by 15 June after financial year end |

| Form 16A | Form 131 | Issue within 15 days of due date for filing TDS return |

If you're an employee

If you're an employer or payroll professional

1. Does this change affect ITR filing for FY 2025-26 (AY 2026-27)?

No. The changes take effect from 1 April 2026, meaning they apply to FY 2026-27 onwards. Your ITR for FY 2025-26 — which most people will file between July and October 2026 — will still reference the old form numbers. Form 16 will still be called Form 16 for that year.

2. Will the Income Tax portal be updated automatically?

Yes, the portal will reflect the new form names once the rules come into effect. You'll see Form 130 and Form 168 in your profile rather than Form 16 and Form 26AS. The underlying data and access process remain the same.

3. Do I need to resubmit or refile anything because of this change?

No. This is a naming change, not a structural or data change. No resubmission is required. Previously issued Form 16s remain valid for the years they were issued.

4. My tax consultant still refers to Form 16. Should I be concerned?

For FY 2025-26 filings, Form 16 is still the correct reference — the change only applies from FY 2026-27. If your consultant is preparing FY 2026-27 returns and still using the old names after April 2026, it's worth flagging. In practice, most professionals will adapt quickly once the new rules are in effect.

5. Why do the new form numbers jump from 16 to 130?

The new numbering follows the structure of the Draft Income Tax Code, which organises provisions and forms into a different sequence than the 1961 Act. The numbers are not arbitrary — they map to specific sections within the new Code. The jump from familiar two-digit numbers to three-digit ones reflects that reorganisation.

A form rename is one of the less dramatic things that can happen in tax law — but it's also exactly the kind of change that causes disproportionate confusion if people aren't prepared for it. The first June after the transition, there will be employees asking why they haven't received their Form 16, not realising it's now called Form 130. There will be payroll teams filing returns under old form numbers. There will be ITR filings with mismatched references.

None of that is complicated to avoid. It just requires knowing the change is coming.

FY 2026-27 is when the new names go live. The time to update your references, your systems, and your team's awareness is now — not during filing season when the pressure is already on.

Need help preparing your organisation for the FY 2026-27 tax form transition?

GA Consulting helps businesses stay ahead of tax and compliance changes — from payroll system audits to employee communication frameworks. If your organisation needs support preparing for the FY 2026-27 transition, reach out to our team.

→ Reach out to GA Consulting today for a free consultation.

We are driven by our Organizational strategy for ‘GA Consulting’ that outlines the journey we embarked,

what we want to achieve and what we want to uphold in this process.

© 2026 GA Consulting - All Rights Reserved - Designed & Developed by GA Digital Solutions

* Privacy Policy